Part III: An Investment Strategy Resistant to Market Crashes

Part III: An Investment Strategy Resistant to Market Crashes

Why & how to rebalance, an exit strategy for your investments, plus Sunday Assorted Links #9: Techno-optimism, Unschooling, and more!

This newsletter helps you travel digitally. Every week, you will receive a list of places to visit on the internet curated by me. Also, this newsletter is how I am figuring out life. If interested, subscribe below. Happy travels!

In Part I, we saw what the Permanent Portfolio (PP) strategy is and how it helps you weather market crashes. In Part II, we saw how and where one should invest in order to implement this strategy.

In case you missed it (or forgot), we split the implementation into 3 steps:

1️⃣ Investing (covered in Part II)

2️⃣ Rebalancing

3️⃣ Exiting.

Today, we will be looking at rebalancing and exiting. Rebalancing is the cornerstone of not just the permanent portfolio but of any investment portfolio. You are not going to want to miss this.

Disclaimer: I am no financial expert and I am not responsible for any losses you incur. Please consult with your investment advisor before you invest in any of the instruments mentioned below (they carry significant risk).

Let’s jump into it.

⚖ Rebalancing ⚖

Rebalancing is the act of withdrawing from over-allocated asset classes and re-investing in under-allocated asset classes. Without rebalancing, your corpus will turn volatile. From my previous article:

Even if you invest in 25:25:25:25 ratio, you will fail to reap the benefits of the PP if you do not rebalance. Let’s say you keep investing in that ratio without rebalancing; in a few years, your equity will swell to 60% of your portfolio. Now, say there is a market crash. You will lose this 60% and whine like a baby.

Rebalancing is not limited to Permanent Portfolio (PP), it is a universal strategy for minimizing risk.

Say you chose a 60-40 portfolio i.e 60% equity and 40% debt. You keep investing without rebalancing periodically (to bring it back to 60:40). Since equity grows quickly, it will eventually balloon to 90% of your portfolio. It would be delusional to think that you have 40% of your money in safe, non-volatile instruments. You don’t. You only have 10%.

Rebalancing is how you solve this ballooning problem. You divest from equity so that it comes back to 60% and you invest that amount in debt to make it 40%.

1. Types of rebalancing

There are two types of rebalancing:

✅ Systematic: Rebalancing at a particular frequency (yearly, half-yearly, quarterly, weekly)

✅ Trigger: Rebalancing whenever your portfolio deviates by x% (a trigger) from the desired allocation

The simplest rebalancing strategy is to do it yearly and whenever there is a 5% deviation. There are different strategies that ask you to rebalance at different frequencies and at different trigger levels. But for the sake of simplicity, I stick to yearly rebalancing with a 5% trigger. (If interested, you can see the comparison of various rebalancing strategies here.)

The next question is….

2. 🤔How to rebalance?🤔

Rebalancing is simple. Not easy, but simple.

First, let us set some things up so that it makes it easier for us to do the rebalancing.

2.1 The Setup

⏩ Create a Portfolio Tracker.

It is a simple spreadsheet that has each of the asset classes that you have invested in. Now, you track your portfolio by checking what the current value of your investment is for each asset class. Example:

This also gives you an overview of how much savings you have in total.

⏩ Fix a date to track your portfolio every month.

This is called the Portfolio Tracking Date (PTD). For example, my PTD is the last weekend of every month.

Let us look at how to do both kinds of rebalancing i.e 5% trigger + yearly.

2.2 Trigger Rebalancing

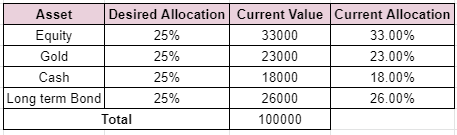

I keep tracking my portfolio every month on the PTD, noting down how much each of my assets is worth. On a particular month, I find the below scenario:

There is more than a 5% deviation in a bunch of asset classes. My trigger criterion of 5%-deviation has been met which means it’s time to rebalance. I would carry out the following actions:

Withdraw 8000 from equity and 1000 from long term Govt bond

Invest 2000 in gold and 7000 in cash

And voila.

If there is still a small deviation of around 1%, it is alright. Don’t fuss about it.

🚨Remember🚨

Rebalance whenever there is a huge market event like the COVID market crash. It is most likely that your trigger condition has been met. Do not wait until your PTD.

2.3 Systematic Rebalancing

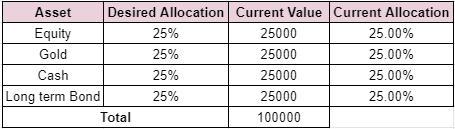

Pick a month that is comfortable for to carry out this activity. On this month each year, calculate the current allocation, and no matter the deviation, rebalance it to achieve your original allocation.

2.4 Common pitfalls to avoid

⛔ Do not try to time the market. When you rebalance, simply withdraw from over-allocated funds in one shot, and invest that money into underallocated funds.

⛔ Do not try and bring your overall portfolio allocation to 25-25-25-25 by adjusting the amount you invest each month. Bringing back to that ratio is the purpose of rebalancing, not of investing. When you are investing, forget about the current allocation and invest according to the desired allocation.

⛔ Do not put off rebalancing so as to avoid STCG and exit load. Stick to the period of 1 year + 5% trigger and rebalance anyway. It’s hard, I know. I too was hesitant to do it in the beginning. But it’s a small price to pay for stable and reliable wealth creation. Don’t be penny wise and pound foolish.

2.5 Problems with Rebalancing

Consider this scenario:

You check your asset allocation on the PTD

You notice that there is more than 5% and you decide to rebalance

You withdraw from over-allocated assets on PTD

You get the money from the fund houses into your account only on PTD+4 or PTD+5

Once you get the money, you invest in other under-allocated instruments to rebalance

But in those 5 days, the market would have shifted quite heavily that even after rebalancing, you are left with quite a bit of deviation (less than 5% however)

This is annoying. But we can tackle this. There are two options:

💧 You can park some buffer money in a liquid fund (a ‘rebalancing pool’ of sorts) that you can use as a cushion when you rebalance. On the day of rebalancing, you withdraw the required amount from this pool and invest in assets that are under-allocated. That way, you do not have to wait for 5 days until the fund house credits the amount into your account. Whenever you do receive the amount, replenish the rebalancing pool.

🚑 Instead of creating a new rebalancing pool, you can re-purpose your emergency fund. The chances of one needing the emergency fund in that 5-day window is low so might as well device more value out of that fund.

This latter is a better option because keeping a large chunk of money idle in a liquid fund (rebalancing pool) is a poor use of that money.

3. 🏃♂️Exiting🏃♂️

Having an entry strategy i.e an investment strategy without an exit strategy is a recipe for financial disaster. But given the low volatility of PP, an exit strategy is not as important. It still is important, just not as important as it would be for other strategies.

Nonetheless, have one in place. If you have a goal in T years from now, start gradually withdrawing money from this portfolio from the T-4 year. You can withdraw 20% of the required amount each year and park that money in a liquid fund like below:

This is just an example. Choose an exit strategy that works the best for you. (You can read further here)

Next week, we will look at variations of the PP and whether you can outsource the implementation.

Check out Part IV here.

This Week’s Interesting Reads

No rabbit hole for this week but we do have lots of interesting places to visit so buckle up!

Leo Babauta on Zen Habits, Antifragility, Contentment, and Unschooling

By Tim Ferriss

Podcast | 1 hr 34 min listen | Tags: Habits, Productivity, Parenting

I have long been interested in the concept of unschooling but never got around to reading about it (because I am not going to be a parent anytime soon). But this conversation between these two smart folks helped me understand the basics of it. As someone who has undergone and has seen his friends undergo the quarter-life career-crisis, unschooling is something I strongly support. From the podcast:

"School in a lot of ways is about conformity. It's not so much about how much you've learned but it's about how well you're following the rules.

And so the idea behind unschooling is that you’re learning in the same way that you and I do today, Tim, as adults. You and I have not stopped just because we’re out of school, we haven’t stopped learning. We’re actually probably learning more than we did when we were in school. But we’re learning on our own terms because we are motivated by it, at our own pace, with our own structure. And that’s what unschooling, is empowering the kids to actually decide for themselves what they care about, what they want to learn. And what that means is that they’re not going to necessarily learn everything that everyone is, quote, “supposed to learn” by the age of 13. But they would have learned a whole different set of things.

And the really important thing is that actually learning can be incredibly fun. That they learned how to face uncertainty. They learned how to motivate themselves and create their own structure. They learned that it’s okay to give up on learning something if you found something else that you’re more passionate about. They also learned how to hold themselves into learning something when they are feeling discouraged about it. So there’s a whole set of meta-learning that is available to unschoolers that isn’t given to regular schoolers."

Marc Andreessen - Making the Future

By Patrick O'Shaughnessy

Podcast | 1 hr 19 min listen | Tags: Tech, Silicon Valley, Civilization

I turned into a techno-optimist after listening to Marc and the likes. It is always enlightening to listen to and see how Marc thinks because the way he joins the dots is just impossibly impressive. Take for example one of the things he says in this podcast: Software is a lever.

We have stopped innovation in the realm of atoms. For example, cars have been the same for ages now with only minor improvements. But software brought about a radical improvement. Uber is just a piece of software but it helps move atoms - by enabling cars to get to passengers. Software is a lever applied to the real world.

Consider another excerpt from the conversation (paraphrased heavily):

Is tech going to steal jobs? Yes. And that's a good thing.

Consider blacksmiths who put horseshoes on horses. When cars were invented many protested. Some had their lives ruined, some didn't adapt but some went on to find better jobs. Change is inevitable and it's for the good.

Think about the future generations - if you ask a person working in an assembly line if their kid should become a software dev or if they should continue working in assembly line, they're going to pick the former.

We see this with a lot of things today. Take NoCode. Is NoCode stealing the jobs of devs? Yes but no. It has become a skill and domain in itself. Companies now look for candidates who have experience with NoCode tools instead of developers. Jobs are not simply disappearing but are merely changing. This is not surprising - we have been making such transitions ever since we set foot on this planet. As Alfred North Whitehead said, “Civilization advances by extending the number of important operations which we can perform without thinking about them.”

Quote of the week

"You are where you are today because you stand on somebody’s shoulders. And wherever you are heading, you cannot get there by yourself. If you stand on the shoulders of others, you have a reciprocal responsibility to live your life so that others may stand on your shoulders. It’s the quid pro quo of life. We exist temporarily through what we take, but we live forever through what we give."

- Vernon JordanThat’s all for this week!

All views expressed by the author are personal.

Any feedback and criticism are more than welcome. You can reach out to me anytime on Twitter or LinkedIn or Instagram.

Thanks for reading! If you liked it, do share it with your friends and family.

To receive this weekly newsletter in your mailbox every Sunday, subscribe below.