An Investment Strategy Resistant to Market Crashes (Part 1)

Plus! Assorted links #7: How technology is helping us fight loneliness, cognitive blind spots and more!

This newsletter helps you travel digitally. Every week, you will receive a list of places to visit on the internet curated by me. Also, this newsletter is how I am figuring out life for myself. If interested, subscribe below. Happy travels!

I finally found an asset allocation strategy that works for me. It makes the right trade-offs and checks the right boxes. Low volatility - check. Not too time consuming - check. Inflation beating returns - check.

In this 3-part series, I will lay it out in detail. Before we begin, lets address a few key points.

Disclaimer: I am no financial expert and I am not responsible for any losses you incur. Please consult with your investment advisor.

There is no one-size fits all when it comes to personal finance because it is exactly that - personal. The below are the trade-offs I am happy to make and are the factors I care about. If they match your preferences, then this strategy might make sense.

I want to spend as little time as possible handling my finances. I have other interesting things to do in life.

I am not investing to make money. To make money, I would rather spend my time becoming better at my job. I am only trying to beat inflation so that my earnings don’t erode in value.

I like my portfolio lean and clean.

I am looking for long term wealth generation (>10 or 15 years)

Before you read this, make sure you have laid the foundation of your personal finance i.e you have an emergency fund, a health insurance, and a term insurance.

With that long-ass prelude out of the way, lets jump into it.

The Permanent Portfolio

Harry Browne, in his book Fail-Safe investing, lays out a stupidly simple framework to accrue wealth irrespective of the market conditions. Browne posits that one of four types of economic conditions will prevail at any given time:

1️⃣ inflationary boom

2️⃣ inflationary bust

3️⃣ deflationary boom

4️⃣ deflationary bust

Inflation-deflation is when cost of living increases or decreases (respectively).

Boom-bust is when there is a period of economic prosperity or economic recession (respectively).

Your portfolio should have at least one asset class that does well in at least one of these conditions. Given this premise, Browne put together the below and aptly named it the Permanent Portfolio (PP):

✅ 25% in equity (does well during a boom)

✅ 25% in gold (does well during inflation)

✅ 25% in cash (does well during deflation)

✅ 25% in long term government bonds (does well during a recession)

It might seem non-sensical to invest just 25% of one’s money in equity and even more non-sensical to keep 25% of your savings as cash. That was my first reaction too. But the reasoning is irrefutable - you will inevitably go through all the 4 economic conditions so an asset class for each period along with periodical rebalancing will give you stable returns.

What is rebalancing you ask? Rebalancing is like hitting a reset button on your portfolio. Even if you invest in 25:25:25:25 ratio, you will fail to reap the benefits of this asset allocation if you do not rebalance. Let’s say you keep investing in that ratio without rebalancing; in a few years, your equity will swell to 60% of your portfolio. Now, say there is a market crash. You will lose this 60% and whine like a baby. That is the antithetical to PP’s objective. Whine-minimization is The Goal here. More on how you can do this in part 2 (next week).

Why it works

“If I am investing just 25% in equity, am I losing out on returns?” That depends on how greedy you are. You cannot have stability and earth-shattering returns.

Imagine a portfolio with just equity. If the market crashes, your entire corpus crashes too. A good portfolio always has a mix of uncorrelated assets so as to minimize steep drawdowns (declines). PP does precisely this.

Even though all the asset classes apart from cash (i.e gold, govt bond and equity) are highly volatile individually, by putting them together you achieve low volatility. This is the power of combining uncorrelated assets. It is also a live example of why questions like ‘what is the best place to invest?’ don’t make any sense. There is no such thing. An asset class should be judged in the context of the portfolio and should not be judged in isolation.

The below chart by Freefincal compares 5 portfolios in the Indian market: 100% equity (blue), 100% long term government bonds (red), 100% gold (green), 100% cash (purple), 25% in each i.e PP (black)

You can see how stable PP is compared to equity and how it gives better returns than gold, govt bonds and liquid funds. PP remains largely unaffected even during the 2008 market crash and the COVID market crash in March 2020. This means you can dip into your savings at any time no matter the market condition.

PP gives less returns most of the time compared to equity but is less volatile 100% of the time. Stability is the best hedge against unpredictability, recession and crashes.

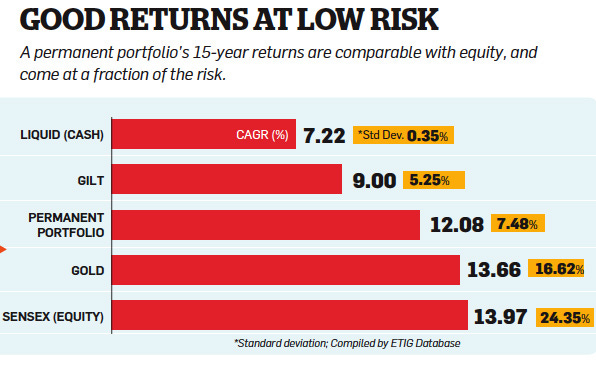

If you look at the standard deviation in this 15 year period, PP is 3x less volatile than equity but it gives 12% while the equity gives 14%.

Not bad at all. I would choose peace of mind over 2% more returns any day. These numbers might change depending on which 15 year period you look at but the point still remains. Low volatility = better liquidity + better sleep.

Next week, we will look at how you can get started with this asset allocation.

Check out Part II here.

Further Reading

The Permanent Portfolio Investing Strategy

By Josh Kaufman

Blog | 6 minute read | Tags: Personal Finance

This is a better introduction to Permanent Portfolio by Josh. This article introduced me to this strategy and it outlines the bull case for this strategy much better than I do.

The Farmer’s Fable: Free as in Lunch

By Taylor Pearson

Blog | 8 minute read | Tags: Personal Finance

I was initially hesitant to rebalance and this article was like a slap on the face. Once you understand how it helps in corpus building, you won’t turn back. Taylor explains it using an analogy so even noobs like myself understand it easily. If you’re a noob too, don’t miss this.

Other Interesting Reads

How the Internet Is Reacting to the Loneliness Epidemic

By Rex Woodbury

Blog | 18 minute read | Tags: Mental Health, Culture, Loneliness, Technology

Rex’s writing, without fail, teaches me something new about the internet and its impact on people and culture. It’s amazing to see how internet is bringing people together. Communities have been on the decline and one of the main drivers is declining belief in theism and religion. People dont congregate at Churches and Temples as much as they used to anymore. However, thanks to internet, we can find communities online and this has been important in the context of this pandemic. While socializing with people on the internet is not the same as meeting your friends at Church on sundays, it is the best we have. (Oh also, this is an example of how bits > atoms.)

Your Brain Overlooks this Problem Solving Strategy

By Scientific American

Blog | 7 minute read | Tags: Mental Health, Culture, Loneliness, Technology

The research findings make it astoundingly clear. We have a bias for solving problems by bringing new elements into the picture than by removing elements. One reason is what the authors say - if we solve the problem by adding something, we get the satisfaction of worked.

I think there is another reason: our mindset when it comes to problem solving. We think of a ‘solution’ as something external to the space in which a problem exists. So in order to solve the problem, we need to bring something from outside to within the problem-space. Instead, we should consciously try to look for solutions within the existing space to counter this cognitive blind spot.

Quote of the week

You’ll never do anything great unless you’re willing to look like an idiot in the short term.

- Shane ParrishThat’s all for this week!

All views expressed by the author are personal.

Any feedback and criticism is more than welcome. You can reach out to me anytime on Twitter or LinkedIn or Instagram.

Thanks for reading! If you liked it, do share it with your friends and family.

To receive this weekly newsletter in your mailbox every Sunday, subscribe below.